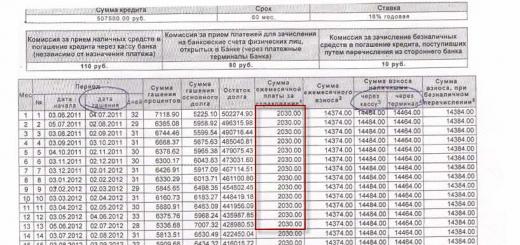

Question 46 financial statements

Reporting year for all organizations is a calendar year - from January 1 to December 31 inclusive.

First reporting year for newly created enterprises - the period from the date of their state registration to December 31. Monthly And quarterly reporting is interim and is compiled on an accrual basis from the beginning of the reporting year. Enterprises submit quarterly financial statements within 15 days after the end of the quarter.

Organizations other than budget present annual financial statements within 90 days tax authorities, as well as at the end of the year in accordance with founding documents founders, participants of the organization or owners of its property (not earlier than 60 days after the end of the reporting year), territorial bodies state statistics at their place of registration.

unitary enterprise having subsidiaries, the terms for compiling and submitting a consolidated annual accounting report are established by the state body or local government authorized to create it.

Joint-stock companies of open type, banks and other credit organizations, insurance companies, exchanges, investment and other funds created at the expense of private, public and state funds (contributions) are obliged publish annual financial statements no later than June 1 of the year following the reporting one.

Enterprises publish financial statements and the final part of the audit report, if this is provided for by the legislation of the Republic of Kazakhstan. Publication is made no later than July 1 of the year following the reporting year, in newspapers, magazines or by distributing brochures, booklets and other publications among users. Consolidated financial statements are signed by the head and chief accountant of the enterprise.

The financial statements of organizations must meet the following basic requirements: reliability, integrity, consistency, comparability, universality of the reporting period, appropriate design and publicity.

Reliability- a complete picture of the property and financial position of the organization, as well as financial results her economic activities. Accounting statements are considered reliable if they are formed and compiled in accordance with the rules established by the regulatory acts of the regulatory system. accounting in the Republic of Kazakhstan.

The reliability of financial statements is enhanced by its integrity, that is, it should include indicators of the financial and economic activities of both the enterprise itself and its branches, representative offices and other structural divisions, including those allocated to independent balance sheets.

The integrity of reporting allows you to make more informed management decisions. To this end, the data of synthetic and analytical accounting must be confirmed by the results of the inventory and the conclusion of an independent audit organization.

Subsequence consolidates in the practice of preparing financial statements the constancy of content and forms balance sheet, income statement and explanations to them from one reporting period to another.

Requirement comparability: the financial statements should provide data on a specific indicator for both the previous and the reporting year. In the event that the data for the period preceding the reporting period are not comparable with the data for reporting period for a number of reasons, the data of the previous period are subject to adjustment according to the established rules.

Requirement generality of the reporting period establishes that for all organizations the reporting year is the period from January 1 to December 31 of the calendar year inclusive.

Decor- the next requirement for financial statements. Reporting, as well as accounting of property, liabilities and business transactions, is carried out in Russian in foreign currency Russian Federation- in rubles. The reporting is signed by the head of the organization and the specialist in charge of accounting.

Publicity financial statements are carried out by organizations, the list of which is regulated by the current legislation. These include open joint-stock companies, credit and insurance organizations, stock exchanges, investment funds and funds created at the expense of private, public and state sources. Publication must be preceded auditing with mandatory approval of the annual report general meeting shareholders.

Internal financial statements are not subject to publication, as they are classified as commercial secrets.

The term "reporting period" is used in accounting and denotes the period of time for which a report is prepared, as well as taxes are levied from the enterprise and from individuals. The main reporting period is a year, intermediate - month and quarter. As a rule, all reports and legal actions are carried out at the end of the reporting year. The reporting period, which begins on January 1 and ends on December 31, is called the calendar reporting period. If it, having the same duration, begins on any other date, then it is called the financial year.

The reporting year in Russia starts on 1.01, while in other countries it can start on 1.04, 1.07 or 1.10. It ends with the reporting date, i.e. the date of the annual report.

Sometimes it is possible to choose an annual reporting period that begins and ends at a time when the level of business activity is low. accounts receivable and inventory (to simplify calculations). In this case, the reporting period coincides with the natural business cycle of the enterprise and is called the natural business year.

When drawing up an interim reporting period, the interval between January 1 and the date on which the interim report is drawn up, inclusive, is considered.

For enterprises and organizations established in a given calendar year in the Russian Federation, the first reporting year is considered to be the interval between the date of their establishment (the date of state registration) and the date of December 31 of the current year. If the organization is registered after October 31, then the end date of the first reporting year is December 31 of the following year.

In case of liquidation or reorganization of the enterprise, the reporting period is taken from January 1 of the given year to the date of liquidation (reorganization).

Interim reporting periods are a calendar month or a quarter, and the corresponding reports are drawn up. For the purposes of accounting for tax liabilities, a period equal to a calendar year is usually taken (except for cases when calculations are carried out according to Changes in the reporting period are possible only with the permission of the tax administration.

In the preparation of financial statements, such a concept as the code of the reporting period is used. This is a two-digit number, put down in a specially designated column of the accounting report. For any reporting period, the code is strictly defined, just as for different types reports. For a complete list, see the codebook.

According to this directory, the numbers from 01 to 12 are codes of reporting periods equal to the corresponding months of the year. 20 - quarterly report code, from 21 to 22 - quarterly report codes from 1st to 4th quarter, respectively, 31 - report code for half a year, 33 - for 9 months, 34 - for a year.

There are other codes corresponding to certain reporting periods. So, when compiling reports for several months, digital designations are used in the range of numbers from 35 to 46.

The handbook also provides cases for compiling accounting reports upon reorganization or liquidation of the enterprise. So, for example, the number 50 in the reporting period code column indicates the last taxable period in the event of liquidation or reorganization of the enterprise. In other cases of reorganization (liquidation), the following designations are used:

Code 51 - report for the 1st quarter;

52 - for half a year;

53 - report for 9 months;

54 - for the 2nd quarter;

55 - for the 3rd quarter;

56 - for the 4th quarter of the year.

In addition, when preparing monthly reports in the event of liquidation or reorganization, numeric codes from 71 to 82 are used to indicate reports for the months from January to December, respectively, and 90 for the year. In the same cases, in reports for the 1st quarter, half a year, 9 months and a year (i.e., when preparing interim reports), codes from 91 to 94 are put down, respectively. Code 99 is provided by the code book for other unplanned cases.

1. The reporting year for all organizations is a calendar year - from January 1 to December 31 inclusive. 2. The first reporting year for newly created organizations is the period from the date of their state registration to December 31 of the corresponding year, and for organizations established after October 1 - to December 31 of the next year. Data about business transactions conducted before the state registration of organizations are included in their financial statements for the first reporting year. 3. Monthly and quarterly reporting is interim and is compiled on an accrual basis from the beginning of the reporting year.

Article 15

1. All organizations, with the exception of budget organizations, submit annual financial statements in accordance with the constituent documents to the founders, participants of the organization or owners of its property, as well as to the territorial bodies of state statistics at the place of their registration. State and municipal unitary enterprises submit accounting reports to the bodies authorized to manage state property. Accounting statements are submitted to other executive authorities, banks and other users in accordance with the legislation of the Russian Federation. 2. Organizations, with the exception of budgetary and public organizations (associations) and their structural subdivisions, which do not carry out entrepreneurial activities and do not have, except for retired property, turnover on the sale of goods (works, services), are required to submit quarterly financial statements within 30 days after the end of the quarter , and annual - within 90 days after the end of the year, unless otherwise provided by the legislation of the Russian Federation (paragraph as amended, entered into force on July 30, 1998 federal law dated July 23, 1998 N 123-FZ, - see the previous edition). The submitted annual financial statements must be approved in the manner prescribed by the constituent documents of the organization. 3. Budget organizations submit monthly, quarterly and annual financial statements to a higher body within the time limits established by it. 4. Public organizations (associations) and their structural units, who do not carry out entrepreneurial activities and do not have turnovers for the sale of goods (works, services) except for the retired property, submit financial statements only once a year based on the results of the reporting year in a simplified composition: a) balance sheet; b) profit and loss statement; c) report on intended use funds received. (The clause is additionally included from July 30, 1998 by the Federal Law of July 23, 1998 N 123-FZ) connections. The user of the financial statements is not entitled to refuse to accept the financial statements and is obliged, at the request of the organization, to put a mark on the copy of the financial statements on acceptance and the date of its submission. Upon receipt of financial statements via telecommunication channels, the user of financial statements is obliged to transfer to the organization a receipt of acceptance in electronic form. The date of submission of financial statements by the organization is the date of dispatch of the postal item with a list of attachments or the date of its dispatch via telecommunication channels or the date of actual transfer by ownership. (Clause as amended by Federal Law No. 32-FZ of March 28, 2002, put into effect on April 13, 2002 - see previous version)

Reporting year

- 1. The reporting year for all organizations is a calendar year - from January 1 to December 31 inclusive.

- 2. The first reporting year for newly created organizations is the period from the date of their state registration to December 31 of the corresponding year, and for organizations established after October 1 - to December 31 of the next year.

Data on business transactions carried out prior to the state registration of organizations are included in their financial statements for the first reporting year.

3. Monthly and quarterly reporting is interim and is compiled on an accrual basis from the beginning of the reporting year.

Addresses and deadlines for the submission of financial statements

1. All organizations, with the exception of budget organizations, submit annual financial statements in accordance with the constituent documents to the founders, participants of the organization or owners of its property, as well as to the territorial bodies of state statistics at the place of their registration. State and municipal unitary enterprises submit accounting reports to the bodies authorized to manage state property.

Accounting statements are submitted to other executive authorities, banks and other users in accordance with the legislation of the Russian Federation.

2. Organizations, with the exception of budgetary and public organizations (associations) and their structural subdivisions, which do not carry out entrepreneurial activities and do not have, except for retired property, turnover on the sale of goods (works, services), are required to submit quarterly financial statements within 30 days after the end of the quarter , and annual - within 90 days after the end of the year, unless otherwise provided by the legislation of the Russian Federation.

The submitted annual financial statements must be approved in the manner prescribed by the constituent documents of the organization.

- 3. Budgetary organizations submit monthly, quarterly and annual financial statements to a higher body within the time limits established by it.

- 4. Public organizations (associations) and their structural subdivisions that do not carry out entrepreneurial activities and do not have turnovers for the sale of goods (works, services, except for retired property), submit financial statements only once a year based on the results of the reporting year in a simplified composition:

- a) balance sheet;

- b) profit and loss statement;

- c) a report on the intended use of the funds received.

- 5. Financial statements can be presented to the user by the organization directly or transmitted through its representative, sent in the form of a postal item with a list of attachments or transmitted via telecommunication channels.

The user of the financial statements is not entitled to refuse to accept the financial statements and is obliged, at the request of the organization, to put a mark on the copy of the financial statements on acceptance and the date of its submission. Upon receipt of financial statements via telecommunication channels, the user of financial statements is obliged to transfer to the organization a receipt of acceptance in electronic form.

The date of submission of financial statements by the organization is the date of dispatch of the postal item with a list of attachments or the date of its dispatch via telecommunication channels or the date of actual transfer by ownership.

The accounting year is the period during which all necessary records of the company's income and expenses are kept, and then entered into financial statements. The reporting year begins on one day and ends exactly 365 days later: sometimes this figure may vary depending on the height of the year. If the reporting year coincides with the usual dates of January 1 and December 31, then it is equal to the calendar year. In all other cases, it is simply the reporting year and its dating is based on the needs of the company.

In some other countries, the reporting year may start and end on dates other than the calendar year. For example, in the United States, the reporting year is considered to be from October 1 to September 30 of the following year. For many schools, the reporting year starts on July 1 and ends on June 30 in order to better adjust to the operation of the school system.

Companies often keep track of the period depending on their line of business. For example, some businesses start the reporting year on February 1, as they need to wait for the return of purchases after the holidays. IN New Year a lot of goods are sold, and therefore, along with it, the volume of returns from buyers also increases. This decrease in income must be correctly taken into account, and therefore the shift of the reporting year to the beginning of February will be a smart decision for many large companies.

When recording a year for the reporting period, the year that falls on the closing date of the reporting period is selected. Thus, a company with a reporting year of 1 April 2017 to 31 March 2018 would have an entry for the year 2018, even though the period started in 2017.

Who and how should choose the dates for the reporting year?

Companies whose management structure is shareholders and whose activities are related to the purchase and sale of shares should choose a reporting year coinciding with the calendar year due to the complexity and variety of business processes.

Individual entrepreneurs should also choose reporting in accordance with the calendar year. The entrepreneur is in itself the owner of the business and at the same time is obliged to pay taxes. To combine all these nuances, it is necessary to draw up reports in full in accordance with the calendar year. Then there will be no problems with the tax system.

The same applies to large corporations, which are owned by several persons. Their reporting year must be the same as the reporting year of the company they own jointly or separately. Therefore, the calendar year from January to December is chosen for the preparation of financial statements.

If you do not own a huge corporation, then you must have good reasons for changing the date of the reporting period. They must be provided tax service and obtain permission for further use outside the generally accepted dates of the calendar year.

The nuances of accounting

It's not a secret for anyone: it is sometimes very difficult to work in a seasonal business because of the sharply increasing number of orders. So it is in accounting. Due to the fact that many firms and companies prefer to keep their accounts in accordance with the calendar year, in the last quarter of each year, too much work falls on the shoulders of accountants. This arrangement makes accounting firms introduce a discount system for work during the remaining three quarters. Hence the desire of business leaders to change the dating to other dates for the reporting year appears: after all, in this case, you can get decent savings from year to year on accounting services.